Switzerland is a small, landlocked country located in central Europe. Known for its stunning landscapes, including the Swiss Alps, serene lakes, and picturesque villages, it’s a popular destination for tourists and outdoor enthusiasts. The country is famous for its neutrality, having remained uninvolved in military conflicts for centuries, and is also home to several international organizations, including the Red Cross and many United Nations agencies.

About Switzerland

1. Snapshots

i) Capital: Bern

ii) Currency: Swiss franc (CHF)

iii) Population: ~9.0 million (2025 est.)

iv) Political System: Federal direct democracy with strong cantonal autonomy

v) Global reputation: AAA-rated, stable, innovation & fintech hub; extensive network of double-tax treaties.

2. Competitive Advantages

i) Predictable legal environment and strong rule of law.

ii) Sophisticated banking, wealth-management and fintech ecosystem.

iii) Multilingual workforce (German, French, Italian, English).

iv) Access to EU market via bilateral agreements while staying outside the EU.

v) Tax certainty through advance tax rulings at cantonal level.

4. Banking & Finance Sector

i) Major Institutions: UBS Group (incorporating former Credit Suisse), Julius Baer, Pictet, Lombard Odier.

ii) Strict know-your-customer (KYC) and AML controls; FINMA can confiscate illicit profits (e.g., Julius Baer enforcement 2025).

iii) Deposit insurance scheme protects up to CHF100,000 per client and bank.

3. Legal & Regulatory Framework

i) Federal Constitution + Code of Obligations 2023 (rev.) govern companies.

ii) Swiss Financial Market Supervisory Authority (FINMA) oversees banks, insurers, asset managers and DLT-service providers.

iii) Anti-money-laundering (AMLA) and Automatic Exchange of Information (AEOI) fully implemented.

iv) Switzerland recognises foreign trusts under the Hague Trust Convention (2007) but has no domestic trust law (draft legislation expected 2026).

5. Corporate Governance & Reporting

a) Board: At least one director/signatory resident in CH (for AG/GmbH).

b) Audits:

i) Ordinary – mandatory if two of: >CHF20M assets, >40FTEs, >CHF40M turnover.

ii) Limited – default; may opt-out if <10FTEs and unanimous shareholder consent.

6. Key Authorities & Resources

i) FINMA: www.finma.ch.

ii) Federal Tax Administration (FTA): www.estv.admin.ch.

iii) Cantonal Tax Offices: 26 Cantons.

iv) Swiss Federal Department of Finance (FDF): OECD minimum tax updates.

7. Quick Takeaways

i) Switzerland remains a premier jurisdiction for international holding, financing and IP management structures thanks to competitive effective tax rates, robust treaty access and legal certainty.

ii) Upcoming 15% global minimum tax rules mainly affect large multinationals; SME and private wealth structures remain attractive under existing cantonal regimes.

iii) Absence of a domestic trust law is offset by recognition of foreign trusts; new Trust Act will add optional local trust regime.

iv) Efficient formation (˜2 weeks) and moderate share-capital thresholds (CHF 20k/100k) make Swiss vehicles accessible to a broad range of investors.

History

History

1. Prehistoric and Roman Era (before 5th century AD)

i) Prehistoric Settlements: Evidence of human habitation dates back to the Paleolithic era. Later, Celtic tribes, especially the Helvetii, inhabited the area.

ii) Roman conquest:

Around 15 BC, the Romans conquered the region, integrating it into the Roman Empire as part of Raetia and Germania Superior. They built roads, towns (like Aventicum, now Avenches), and infrastructure.

History

2. Early Middle Ages (5th–10th Century)

i) After the fall of the Roman Empire, Germanic tribes such as the Alemanni and Burgundians settled in the area.

ii) The territory became part of the Frankish Empire under Charlemagne and later split under the Treaty of Verdun in 843 AD.

History

3. High Middle Ages (11th–13th century)

i) The region was part of the Holy Roman Empire.

ii) Powerful feudal families, especially the Habsburgs, began to dominate the region.

History

4. Formation of the Swiss Confederation (1291–1499)

i) 1291:

The traditional founding date of Switzerland, when the cantons of Uri, Schwyz, and Unterwalden formed a defensive alliance.

ii) Over time, more cantons joined the Old Swiss Confederacy.

iii) Battle of Morgarten (1315) and Battle of Sempach (1386) marked Swiss victories over the Habsburgs.

iv) 1499:

The Swabian War ended with Swiss independence from the Holy Roman Empire (de facto, not formal yet).

History

5. Reformation and Religious Wars (16th–17th century)

i) Ulrich Zwingli and John Calvin led the Protestant Reformation in parts of Switzerland.

ii) Switzerland became religiously divided: some cantons remained Catholic, others became Protestant.

iii) A series of internal religious conflicts followed, including the Kappel Wars.

History

6. Napoleonic Era & the Helvetic Republic (1798–1815)

i) 1798:

France invaded and established the Helvetic Republic, a centralized state replacing the loose confederation.

ii) 1803:

Napoleon’s Act of Mediation restored some autonomy to the cantons.

iii) 1815:

After Napoleon’s defeat, the Congress of Vienna reaffirmed Swiss neutrality and independence, and added Valais, Neuchâtel, and Geneva as cantons.

History

7. Modern Federal State (1848–present)

i) 1848:

After a brief civil war (Sonderbund War), Switzerland adopted a federal constitution, establishing the modern Swiss Confederation with a strong central government.

ii) 1874:

The constitution was revised to give more power to the federal government and introduced direct democracy tools (referenda and initiatives).

iii) 20th Century:

Switzerland remained neutral in both World Wars but served as a diplomatic and humanitarian hub.

iv) 2002:

Switzerland joined the United Nations.

v) Today, Switzerland is known for its neutral foreign policy, direct democracy, multilingualism (German, French, Italian, Romansh), and high standard of living.

Economy

Switzerland has one of the most stable and prosperous economies in the world. Here's a high-level overview of its key economic features:

1. General Economic Characteristics

i) Type:

Highly developed, free-market economy

ii) GDP (nominal):

~$900+ billion USD (2024 est.)

iii) GDP per Capita:

~$100,000 USD — among the highest globally

iv) Currency:

Swiss Franc (CHF) — known for its stability

2. Key Sectors

i) Banking & Finance:

One of the world’s leading financial hubs (Zurich & Geneva are major global financial centers)

ii) Pharmaceuticals & Life Sciences:

Home to giants like Novartis and Roche

iii) Machinery & Precision Instruments:

Renowned for high-quality exports like watches (e.g., Rolex, Patek Philippe)

iv) Tourism:

Significant contributor, especially from alpine and luxury tourism

v) Agriculture:

Small part of GDP but protected and efficient — known for dairy, cheese, and chocolate

3. Trade

i) Exports:

Pharmaceuticals, machinery, chemicals, watches, financial services

ii) Main Export Partners: Germany, United States, China, France, Italy

iii) Imports:

Machinery, chemicals, vehicles, metals, agricultural products

4. Labor Market

i) Low Unemployment Rate:

~2–3% (among the lowest in Europe)

ii) High productivity and wages

iii) Multilingual and highly skilled workforce

5. Economic Strengths

i) Political and economic stability

ii) Strong education system and innovation culture

iii) Favorable tax environment for businesses

iv) Global hub for arbitration and international organizations

6. Challenges

i) High cost of living and doing business

ii) Aging population and pension sustainability

iii) Dependence on exports (vulnerable to global trade tensions)

iv) Housing market tensions in urban areas

Swiss Jurisdiction

Switzerland offers various types of company jurisdictions, each with its specific legal, financial, and operational advantages. Below are the main company structures used in Switzerland.

Key Features of Swiss Offshore Jurisdiction

2. Public Limited Company (PLC) – AG / SA

i) Popular For:

Larger businesses, international trade, or public companies.

ii) Liability:

Limited to the capital invested.

iii) Capital Requirement:

CHF 100,000 minimum, with at least CHF 50,000 paid up.

iv) Management:

Must have a board of directors; one director must be a Swiss resident.

v) Taxation:

Similar to LLCs, subject to federal and cantonal taxation.

1. Limited Liability Company (LLC) – GmbH / Sàrl

i) Popular For:

Small to medium-sized businesses.

ii) Liability:

Limited to the capital invested in the company.

iii) Capital Requirement:

CHF 20,000 minimum.

iv) Management:

Must have at least one managing director, who does not need to be a Swiss resident.

v) Taxation:

Subject to Swiss corporate tax rates, which vary by canton (taxation is federal and cantonal).

3. Branch of a Foreign Company

i) Popular For:

International companies seeking to establish a presence in Switzerland without creating a separate legal entity.

ii) Liability:

The foreign parent company assumes liability.

iii) Management:

Managed by a Swiss representative.

iv) Taxation:

Subject to Swiss taxation on the income generated in Switzerland.

4. Sole Proprietorship

i) Popular For:

Independent professionals, small businesses.

ii) Liability:

Unlimited personal liability of the owner.

iii) Capital Requirement:

No minimum capital required.

iv) Taxation:

Profits are taxed at the personal income tax level.

5. Cooperative – Genossenschaft

i) Popular For:

Groups with common goals, such as mutual benefits, social enterprises, or non-profit organizations.

ii) Liability:

Typically limited to members' shareholding.

iii) Capital Requirement:

No minimum capital, but members contribute.

iv) Taxation:

Subject to corporate tax rules.

6. Key Jurisdictions for Incorporation:

i) Canton of Zug:

Known for its business-friendly environment, low taxes, and a popular choice for international companies, especially in the tech and Blockchain sectors.

ii) Canton of Zurich:

The financial hub of Switzerland, offering well-developed infrastructure and a high level of international connectivity.

iii) Canton of Geneva:

Preferred for companies involved in international trade or with a focus on international clients.

While Switzerland may not be an "offshore" jurisdiction per se, it offers many advantages for international businesses looking for a stable, well-regulated environment with favorable tax conditions.

Taxation

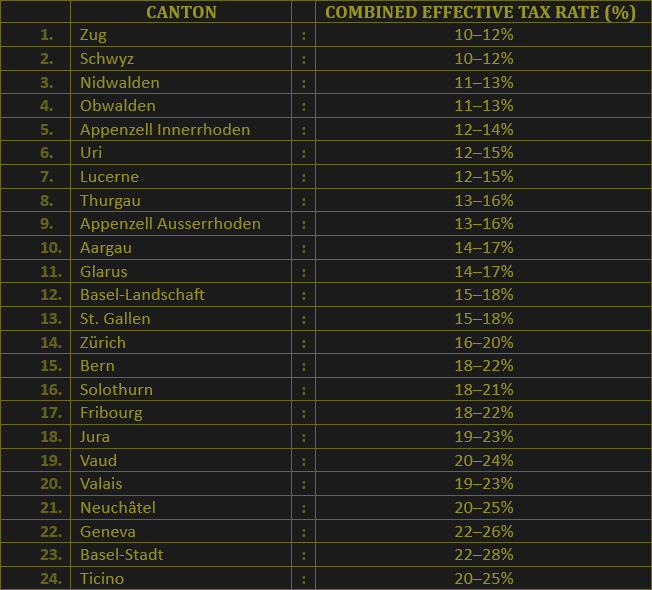

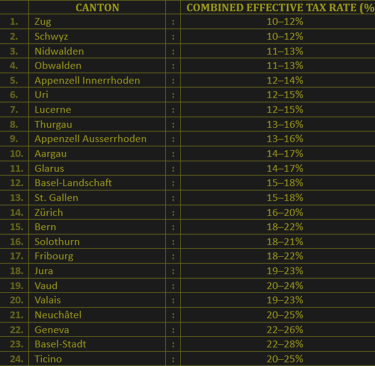

Switzerland's corporate tax system comprises federal, cantonal, and communal taxes, resulting in varying effective tax rates across the country's 26 cantons. The federal corporate income tax (CIT) is set at a flat rate of 8.5% on profit after tax, which translates to an effective rate of approximately 7.83% on profit before tax due to its deductibility.

Cantonal and communal taxes are added to the federal rate, leading to overall effective tax rates ranging from 11.9% to 20.5%, depending on the company's location.

As of 2024, the corporate tax rates in Switzerland's cantons are as follows:

All Rights Reserved © 2026